[Majorityrights Central] Explaining about life and the Reduction ad Hitlerum at The Restorationist Posted by Guessedworker on Wednesday, 13 May 2026 23:04.

[Majorityrights Central] Three possible forms of a Ukrainian victory ... and a Russian defeat Posted by Guessedworker on Thursday, 16 April 2026 16:36.

[Majorityrights Central] Empires, the Chinese Mind, a theoretical nationalism of ethnicity Posted by Guessedworker on Saturday, 14 February 2026 01:54.

[Majorityrights News] Moscow Times: Valdai residents report no sign of drones attacking Putin residence Posted by Guessedworker on Tuesday, 30 December 2025 11:33.

[Majorityrights Central] Thoughts on Mark Collett’s strategy for nationalism in the British future Posted by Guessedworker on Friday, 24 October 2025 15:01.

[Majorityrights Central] Principles, parts, processes of ethnic nationalism, Part 1: inflection? Posted by Guessedworker on Thursday, 31 July 2025 12:03.

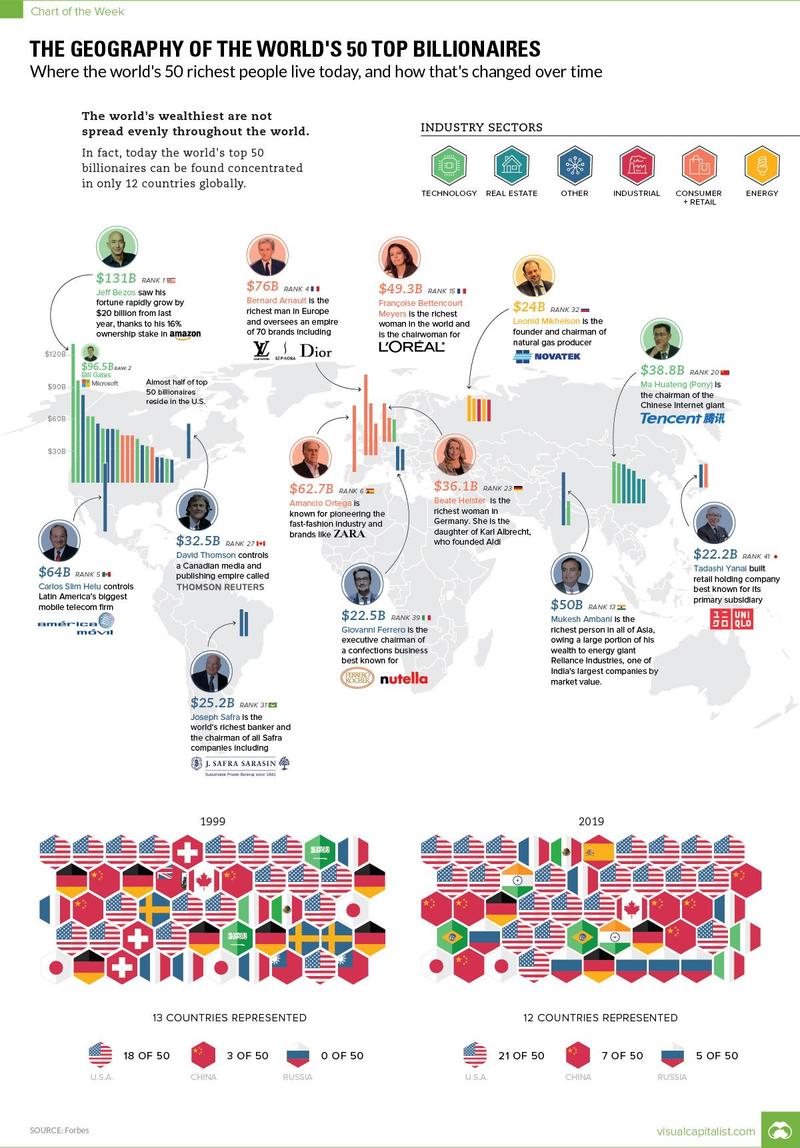

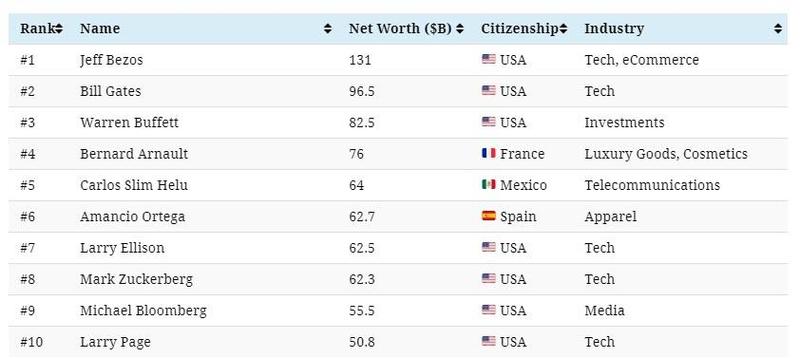

The business world has undergone considerable change in the last two decades.

While some fortunes are always reliably passed on to their respective heirs and heiresses, Visual Capitalist’s Jeff Desjardinsnotes that there are also entirely new industries that rise out of nowhere to shape the landscape of global wealth.

As the wealth landscape shifts, so does its geographical distribution.

We’ll start here by looking at the most recent data from 2019:

The most recent billionaires list features Jeff Bezos at the top with $131 billion, although it’s likely his recent divorce announcement will provide an upcoming shakeup to the Bezos Empire.

Bezos is just one of 21 Americans that find themselves in the top 50 list, which means that 42% of the world’s top billionaires hail from the United States.

Billionaire Geography Over Time

If we compare the top 50 list to that from 1999, it’s interesting to see what has changed over time in terms of geographical distribution. Here’s the distribution of top countries on both lists, compared:

In the last 20 years, Russia and China have stockpiled the most top billionaires, adding five and four to the top 50 list respectively. The United States added three, going from 18 to 21 billionaires over the timeframe. On the other end of the spectrum, Germany, Sweden, and Switzerland have lost the most billionaires from the top 50 ranking.

Russia’s Connection To Brexit Is ‘Opaque And Complicated,’ Journalist Says, NPR, 21 Mar 2019:

Katya Banks

While there are entirely legitimate interests for Britain to leave the E.U., The Russian Federation has had an interest and potential significant influence on the leave campaign as well.

Posted by DanielS on Thursday, 21 March 2019 05:26.

Euro-DNA Nations - [Part 3] healthy self-interest; reaching out to the broad Euro-populations

If our mission to defend European peoples is to be understood and appreciated properly by broad masses enough to gain strength of popularity for success, we must negotiate the common currency of our language.

However, to negotiate that common currency with successful results among the broad masses, our spokesmen and advocates must first of all be disabused of YKW misdirection of terms and concepts of group advocacy so as not to perpetuate social systemic dissolution. By disabusing corrupted terms and concepts and redeploying their corrected proper forms first of all through our spokesmen and dedicated advocates, they can reach out with greater success and popularity to our broader masses to engage in our group systemic homeostasis.

In this discussion with Ecce Lux then, I begin to feel-out a project to rescue terms and concepts that would otherwise structure social systemic homeostasis for European peoples - terms and concepts which have been misrepresented by YKW to tangle, confuse, misdirect and disrupt our group homeostasis.

Our spokesmen and dedicated advocates disabused thus of YKW corrupted terms and concepts first of all and prepared with the proper forms rather for our group homeostatic interests, they can reach out with greater success and popularity to encourage our broader masses to engage defense, fostering and advance of our group interests in coordination and harmony with other peoples - thereby increasing our chances for success as well in that occasion for both intra and intergroup conflict is reduced.

Another red cape they have Whites chasing, I forgot to mention - “equality/inequality”. The matter, rather, for paradigmatic, group management, social systemic homeostasis, is “commensurability/incommensurability”, i.e, do rule structures match and complement the paradigm or not. Casting matters in those qualitative terms allows you to harmonize both intra-group roles and niches AND intergroup relations as you are not rousing conflict and ire through false comparisons which disrespect ecological niche functions.

As alarm bells sound over the advancing destruction of the environment, a variety of Green New Deal proposals have appeared in the U.S. and Europe, along with some interesting academic debates about how to fund them. Monetary policy, normally relegated to obscure academic tomes and bureaucratic meetings behind closed doors, has suddenly taken center stage.

The 14-page proposal for a Green New Deal submitted to the U.S. House of Representatives by Rep. Alexandria Ocasio-Cortez, D-N.Y., does not actually mention Modern Monetary Theory (MMT), but that is the approach currently capturing the attention of the media—and taking most of the heat. The concept is good: Abundance can be ours without worrying about taxes or debt, at least until we hit full productive capacity. But, as with most theories, the devil is in the details.

MMT advocates say the government does not need to collect taxes before it spends. It actually creates new money in the process of spending it; and there is plenty of room in the economy for public spending before demand outstrips supply, driving up prices.

Critics, however, insist this is not true. The government is not allowed to spend before it has the money in its account, and the money must come from tax revenues or bond sales.

In a 2013 treatise called “Modern Monetary Theory 101: A Reply to Critics,” MMT academics concede this point. But they write, “These constraints do not change the end result.” And here the argument gets a bit technical. Their reasoning is that “the Fed is the monopoly supplier of CB currency [central bank reserves], Treasury spends by using CB currency, and since the Treasury obtained CB currency by taxing and issuing treasuries, CB currency must be injected before taxes and bond offerings can occur.”

The counterargument, made by American Monetary Institute (AMI) researchers, among others, is that the central bank is not the monopoly supplier of dollars. The vast majority of the dollars circulating in the United States are created, not by the government, but by private banks when they make loans. The Fed accommodates this process by supplying central bank currency (bank reserves) as needed, and this bank-created money can be taxed or borrowed by the Treasury before a single dollar is spent by Congress. The AMI researchers contend, “All bank reserves are originally created by the Fed for banks. Government expenditure merely transfers (previous) bank reserves back to banks.” As the Federal Reserve Bank of St. Louis puts it, “federal deficits do not require that the Federal Reserve purchase more government securities; therefore, federal deficits, per se, need not lead to increases in bank reserves or the money supply.”

What federal deficits do increase is the federal debt; and while the debt itself can be rolled over from year to year (as it virtually always is), the exponentially growing interest tab is one of those mandatory budget items that taxpayers must pay. Predictions are that in the next decade, interest alone could add $1 trillion to the annual bill, an unsustainable tax burden.

To fund a project as massive as the Green New Deal, we need a mechanism that involves neither raising taxes nor adding to the federal debt; and such a mechanism is proposed in the U.S. Green New Deal itself—a network of public banks. While little discussed in the U.S. media, that alternative is being debated in Europe, where Green New Deal proposals have been on the table since 2008. European economists have had more time to think these initiatives through, and they are less hampered by labels like “socialist” and “capitalist,” which have long been integrated into their multi-party systems.

A Decade of Gestation in Europe

The first Green New Deal proposal was published in 2008 by the New Economics Foundation on behalf of the Green New Deal Group in the U.K. The latest debate is between proponents of the Democracy in Europe Movement 2025 (DiEM25), led by former Greek finance minister Yanis Varoufakis, and French economist Thomas Piketty, author of the best-selling “Capital in the 21st Century.” Piketty recommends funding a European Green New Deal by raising taxes, while Varoufakis favors a system of public green banks.

PRIME Minister Theresa May’s Brexit deal has been rejected by the House of Commons with a 149 majority leaving the future of Britain’s exit from the bloc in complete turmoil.

A hoarse-sounding Mrs May suffered a defeat of 242/391 with a majority of 149 at tonight’s meaningful vote on her deal. She had lost her voice after a late-night flight to Strasbourg to demand concessions on her deal with European Commission president Jean Claude Juncker last night. Though it was not enough to win over both hard-line Brexiteers and MPs that back a People’s Vote. MPs could now vote to delay Brexit following an amendment by Labour’s Yvette Cooper, tabled last month, allowing them to do so.

No deal Brexit BOOST: Jacob Rees-Mogg explains ‘exception’ of no deal

Mrs May also said that “voting against a deal does not solve the issues we face”.

European Commission president Mr Juncker had already warned that if MPs turned down the package agreed in Strasbourg on Monday, there would be “no third chance” to renegotiate.

MPs will vote tomrorow on whether they want to leave the European Union without a Withdrawal Agreement and Political Declaration - a no-deal Brexit.

Should MPs reject that, there will be another vote on whether Parliament wants to seek an extension to Article 50 - delaying the UK’s departure beyond the current March 29 deadline.

But Mrs May stressed that would not resolve the divisions in the Commons and could instead hand Brussels the power to set conditions on the kind of Brexit on offer “or even moving to a second referendum”.

“Quantitative easing” was supposed to be an emergency measure, but the Federal Reserve is now taking a surprising new approach toward the policy. The Fed “eased” shrinkage in the money supply due to the 2008-09 credit crisis by pumping out trillions of dollars in new bank reserves. After the crisis, the presumption was the Fed would “normalize” conditions by sopping up the excess reserves through “quantitative tightening” (QT)—raising interest rates and selling the securities it had bought with new reserves back into the market.

The Fed relentlessly pushed on with quantitative tightening through 2018, despite a severe market correction in the fall. In December, Fed Chairman Jerome Powell said QT would be on “autopilot,” meaning the Fed would continue to raise interest rates and sell $50 billion monthly in securities until it hit its target. But the market protested loudly to this move, with the Nasdaq composite index dropping 22 percent from its late-summer high.

Worse, defaults on consumer loans were rising. December 2018 was the first time in two years that all loan types and all major metropolitan statistical areas showed a higher default rate month over month. Consumer debt—including auto, student and credit card debt—is typically bundled and sold as asset-backed securities similar to the risky mortgage-backed securities that brought down the market in 2008 after the Fed had progressively raised interest rates.

Powell evidently got the memo. In January, he abruptly changed course and announced QT would be halted if needed. On Feb. 4, Mary Daly, president of the Federal Reserve Bank of San Francisco, said it was considering going much further. “You could imagine executing policy with your interest rate as your primary tool and the balance sheet as a secondary tool, one that you would use more readily,” she said. QE and QT would no longer be emergency measures but would be routine tools for managing the money supply. In an article on Seeking Alpha titled “Quantitative Easing on Demand,” Mark Grant writes:

If the Fed does decide to pursue this strategy it will be a wholesale change in the way the financial system in the United States operates and I think that very few institutions or people appreciate what is taking place or what it will mean to the markets, all of the markets.

The Problem of Debt Deflation

The Fed is realizing that it cannot bring its balance sheet back to “normal.” It must keep pumping new money into the banking system to avoid a recession. This naturally alarms Fed watchers worried about hyperinflation. But QE need not create unwanted inflation if directed properly. The money spigots just need to be aimed at the debtors rather than the creditor banks. In fact, regular injections of new money directly into the economy may be just what the economy needs to escape the boom and bust cycle that has characterized it for two centuries. Grant concludes his article by quoting Abraham Lincoln:

The Government should create, issue, and circulate all the currency and credits needed to satisfy the spending power of the Government and the buying power of consumers. By the adoption of these principles, the taxpayers will be saved immense sums of interest. Money will cease to be master and become the servant of humanity.

The quote is apparently apocryphal, but the principle still holds: new money needs to be regularly added to the money supply to avoid an overwhelming debt burden and allow the economy to reach its true productive potential. Regular injections of new money are necessary to avoid something economists fear even more than inflation—the sort of “debt deflation” that took down the economy in the 1930s.

Most money today is created by banks when they make loans. When overextended borrowers pay down old loans without taking out new ones, the money supply “deflates” or shrinks. Demand shrinks with it, and businesses lacking customers close their doors, in the sort of self-feeding death spiral seen in the Great Depression.

The essence of Slavery is that someone else controls the value of our production.

Under Capitalism, people depending on a wage (the 90/99%), typically consume only about 10% of the value of their own production. The entire System is geared to sucking up our production with unearned income: Usury, Landlordism, Speculation, high prices of Monopoly.

In Capitalism, this was achieved by first driving the common people off their ancestral lands by systematically destroying the abundant money systems of the medieval era by forcing Gold Standards everywhere.

This caused a deflation that first savaged the countryside.

In this way, the People lost their means of independence and were forced to work for others for a living, in the cities. Instead of being independent farmers and craftsmen, they were demoted to wage slavery.

By giving him a wage, immediately a large chunk of the value of the worker’s production is taken by the shareholder. The value of the worker’s production is always much higher than his wage.

With Multinationals, profits and shareholder dividends are typically higher than the cost for labor. More than half of the workers’ production is taken by the owners of the company.

Broken

They get away with this because Capital is kept artificially scarce, both through Cartels and through the artificial scarcity of money. In this way, Labor is oppressed, forcing them into low wages and humiliating conditions. With a decent monetary system, not Capital, but Labor would be the scarce factor of production, and men would be either self-employed or co-owner in larger corporations.

The worker receives his wage, and the remaining value of his production is next sucked up with scientific precision.

A wage slave making $2000 per month has a budget something like this: $300 for the State $700 for the Landlord $100 for Energy $200 for ‘health’ ‘care’ $150 for Transportation $50 for Telecom Total: $1500

What remains, $500, about a quarter, is to eat and try to live a life. A fraction of what 40 hours work produced, at least $4000 worth.

The beauty of the System is, that when wages rise, prices, debts (and associated usurious cost), rents, rise along, sucking up the extra purchasing power.

The residual wealth that the Middle Class retains during booms is disowned a little later with the inevitably following crunch, forcing them into liquidation at depressed prices.

Free Markets, Right?! Supply and demand! All good and dandy, we think. Fair enough. We use stuff, so we pay.

But when we take a closer look at where all this money ends up, it transpires that all supply chains we depend on (energy, automotive industry, telecom, ‘health’ ‘care’) are dominated by massive International Cartels.

Cartels keep supply low, and prices high, so a lot of their profits are unearned income, not really related to their production, but to their market power. They use this to keep competitors out, and the Capitalist’s core value is ‘Competition is Sin’ (John D. Rockefeller).

LANDLORDISM

What is more, a great many people are enslaved by Landlordism, which is a vicious Tyranny, first established by the Sword, later overtaken by mortgages, the Money Power’s method of disowning the Landed Aristocracy.

Landlordism is pure parasitism, and all the Land is owned by a really very small group of mostly very old families. For instance: all the homeowners in Britain combined own only 6% of the Land. All the rest is in the hands of a minute percentage of the population. Many of the main Landholders go back all the way to William the Conqueror.

Filthy rich

Usury massively raises all these prices. As we know, Usury is about 40% of prices we pay for all goods and services: cost for capital passed on by the supplier.

This includes the land we live on, and on which we are utterly dependent. In fact, Usury actually QUADRUPLES Landlordism´s rents.

But this is not the only way International Finance profits from everything: they also have a decisive stake in most of the Transnationals that dominate the supply chains we are completely dependent upon. Only 20% of Transnationals (there are about 40,000 of them) are independently owned.

CONCLUSION

In the past, people enslaved in the mines and the sweatshops, say late 19th century Britain, they were even forced by their employers to do their groceries in factory owned shops that charged outrageous prices.

We think we have outgrown this. It’s really time to think again: all that has happened is that Capital (Finance) has upped their game. Local shops on factory compounds are now international supermarket chains. But they are owned by the same people and serve the exact same purpose: reclaiming capital’s losses to wages, usurping our production.

People even go so far as to say ‘Capitalism has lifted people out of poverty’! What is so insane about this, is that a man, in 1694, worked about 15 weeks per year on his own farm. Then with the ascent of Capitalism, two centuries later, he worked 80 hours per week in some soul-crushing ‘job’, and it was still not enough: his wife and his kids had to work too, just to pay for the rent and some potatoes.

Anthony Migchels

Even today, we work at least twice as much as three centuries ago.

The most galling of it all is that people claim ‘freedom’ because once every four years they get to give what remains of their power away to some Kleptocrat insider with ‘democratic elections’.

This is the reality of Capitalism, which is centred around International Finance and its Usury (Banking).

No solution to all this is thinkable, without the end of Usury by interest-free credit for the People.

Brexit Horror: Remainers plot take-over.

Brexit Horror: Remainers plot take-over.

Ellen Brown is an attorney, chairman of the Public Banking Institute; author of twelve books including “Web of Debt” and “The Public Bank Solution.”

Ellen Brown is an attorney, chairman of the Public Banking Institute; author of twelve books including “Web of Debt” and “The Public Bank Solution.”

Abolished

Abolished Broken

Broken Filthy rich

Filthy rich Anthony Migchels

Anthony Migchels