[Majorityrights Central] Explaining about life and the Reductio ad Hitlerum at The Restorationist Posted by Guessedworker on Wednesday, 13 May 2026 23:04.

[Majorityrights Central] Three possible forms of a Ukrainian victory ... and a Russian defeat Posted by Guessedworker on Thursday, 16 April 2026 16:36.

[Majorityrights Central] Empires, the Chinese Mind, a theoretical nationalism of ethnicity Posted by Guessedworker on Saturday, 14 February 2026 01:54.

[Majorityrights News] Moscow Times: Valdai residents report no sign of drones attacking Putin residence Posted by Guessedworker on Tuesday, 30 December 2025 11:33.

[Majorityrights Central] Thoughts on Mark Collett’s strategy for nationalism in the British future Posted by Guessedworker on Friday, 24 October 2025 15:01.

[Majorityrights Central] Principles, parts, processes of ethnic nationalism, Part 1: inflection? Posted by Guessedworker on Thursday, 31 July 2025 12:03.

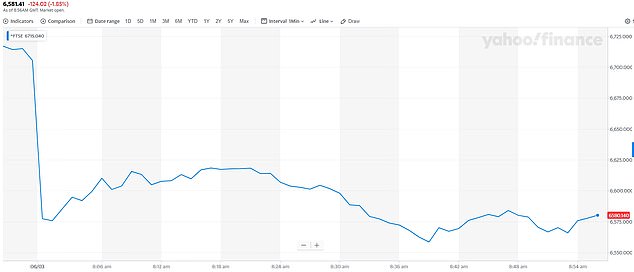

Britain is now facing a ‘recession’ as first coronavirus death on UK soil sends markets in panic with FTSE 100 opening 1.85% down at 6,581 - wiping off gains made during the week

London FTSE100 index major companies loses 124 points, 1.85% to 6,581

Frankfurt DAX30 sheds 1.8% to 11,735, Paris CAC40 drops 1.8% to 5,264

Milan’s major stock index FTSE-Mib also goes down 3.1% to 20,890 points

Hong Kong & Shanghai stocks also tanked overnight amid economic fears.

European stock markets including the FTSE 100 sank further this morning as traders feared that the coronavirus crisis could plunge Britain into recession.

London‘s benchmark index of major companies lost 124 points or 1.85 per cent to 6,581 today after Britain recorded its first death from the infection.

It also comes as a top investment bank warned coronavirus could push the UK to the brink of recession in the coming months.

In eurozone, Frankfurt DAX30 shed 1.8% to 11,735 points and ParisCAC 40 dropped 1.8% to 5,264, compared with yesterday’s closing levels.

TODAY: London’s FTSE 100 of major companies lost 124 points or 1.85 per cent to 6,581 today

THIS WEEK: The FTSE fell this morning, wiping out the gains it had seen so far this week

PAST FORTNIGHT: The FTSE has plunged since the virus sparked a worldwide rout last week

Meanwhile Milan’s major stock index the FTSE-Mib went down 3.1 per cent to 20,890 points as Italy continues to face the biggest outbreak in Europe so far.

In Asia, Hong Kong and Shanghai stocks also tanked as the coronavirus crisis overshadows government and central bank moves to limit economic impact.

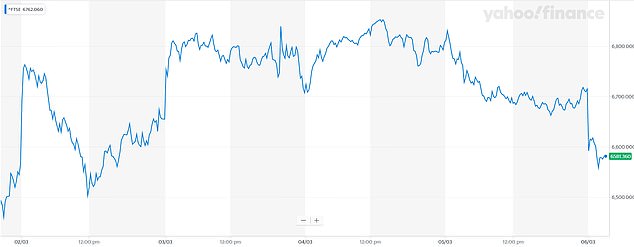

Global markets hit by another wave of panic selling as fears…

for the FTSE 100 erased the index’s gains from earlier this week, with export-heavy companies now having lost more than £175million in value since the epidemic sparked a worldwide rout last week.

Cruise operator Carnival dropped 4.2 per cent to its lowest level since 2012, a day after its Grand Princess ocean liner was barred from returning to its home port of San Francisco on virus fears.

Britain said an older person with underlying health problems had succumbed to the flu-like virus yesterday, while the number of infections jumped to 115.

In company news, drug maker AstraZeneca fell 1 per cent after it said its treatment for a form of bladder cancer failed to meet the main goal of improving overall survival in patients in a late-stage study.

Top investment bank Goldman Sachs analysts has warned coronavirus could push the UK to the brink of recession in the coming months.

They say the outbreak will cause a ‘substantial’ near-term hit to economic growth, decimating the tourism industry and slashing leisure spending as Britons stay indoors.

It will cause a headache for new Chancellor Rishi Sunak, who is due to present his first Budget next week.

But analyst Sven Jari Stehn said: ‘The Budget may now focus on measures to safeguard public health than a broad-based expansion of spending.’

Goldman Sachs expects the economy to be flat in the first three months of 2020 and to contract by 0.2 per cent between April and June.

Posted by DanielS on Wednesday, 19 February 2020 07:13.

Prior to his arrest in 2003 Khodorkovsky (in photo with first Russian President Boris Yeltsin) funded several Russian parties, including the Communist Party, most of which were in competition with each other. Voltairenet.org

A Dutch appeals court on Tuesday (18 February) overturned the annulment of a $50 billion award to shareholders in the now defunct Russian oil giant Yukos, a surprise ruling 13 years after the assets came under control of the Kremlin.

Yukos Oil went bankrupt in 2006 after its former chief Mikhail Khodorkovsky fell out with Russian leader Vladimir Putin and the government began demanding billions of dollars in back taxes that ultimately resulted in its being expropriated by the state.

Tuesday’s verdict reinstates a decision by The Hague-based Permanent Court of Arbitration (PCA) ordering the Russian state to compensate shareholders in the company once headed by fallen oligarch Khodorkovsky. That decision had been overturned in April 2016 by The Hague District Court.

Russia’s Justice Ministry has said it will challenge the appeals court ruling at the Dutch Supreme Court.

“The (lower) court ruled in favour of the Russian Federation, but the court of appeal in The Hague today ruled that the court’s verdict is incorrect. This means that the arbitral award is again in force,” the appeals court said in a statement.

Most of Yukos’ assets were absorbed by the Kremlin’s flagship oil producer Rosneft, and its former owners have for years been trying to recover their possessions.

Legal proceedings seeking damages have been brought by GML, formerly known as Group Menatep Ltd., which held around 70% of shares in Yukos.

Rule of law

Tim Osborne, GML’s chief executive, said the latest ruling was “a victory for the rule of law.”

“The independent courts of a democracy have shown their integrity and served justice. A brutal kleptocracy has been held to account,” he said.

The PCA had ruled in July 2014 that four plaintiffs – not including Khodorkovsky – were entitled to compensation for the loss of their holdings, enabling them to go after Russian state assets.

Russian government assets in France and Belgium including bank accounts have been frozen in a row over compensation for shareholders of defunct oil giant Yukos, officials and a claimant representative said yesterday (18 June).

While US advocates and local politicians struggle to get their first public banks chartered, Mexico’s new president has begun construction on 2,700 branches of a government-owned bank to be completed in 2021, when it will be the largest bank in the country. At a press conference on Jan. 6, he said the neoliberal model had failed; private banks weren’t serving the poor and people outside the cities, so the government had to step in.

Andrés Manuel López Obrador (known as AMLO) has been compared to the United Kingdom’s left-wing opposition leader Jeremy Corbyn, with one notable difference: AMLO is now in power. He and his left-wing coalition won by a landslide in Mexico’s 2018 general election, overturning the Institutional Revolutionary Party (PRI) that had ruled the country for much of the past century. Called Mexico’s “first full-fledged left-wing experiment,” AMLO’s election marks a dramatic change in the political direction of the country. AMLO wrote in his 2018 book “A New Hope for Mexico,” “In Mexico the governing class constitutes a gang of plunderers…. Mexico will not grow strong if our public institutions remain at the service of the wealthy elites.”

The new president has held to his campaign promises. In 2019, his first year in office, he did what Donald Trump pledged to do — “drain the swamp” — purging the government of technocrats and institutions he considered corrupt, profligate or impeding the transformation of Mexico after 36 years of failed market-focused neoliberal policies. Other accomplishments have included substantially increasing the minimum wage while cutting top government salaries and oversize pensions; making small loans and grants directly to farmers; guaranteeing crop prices for key agricultural crops; launching programs to benefit youth, the disabled and the elderly; and initiating a $44 billion infrastructure plan. López Obrador’s goal, he says, is to construct a “new paradigm” in economic policy that improves human welfare, not just increases gross domestic product.

The End of the Neoliberal Era

To deliver on that promise, in July 2019 AMLO converted the publicly owned federal savings bank Bansefi into a “Bank of the Poor” (Banco del Bienestar or “Welfare Bank”). He said on Jan. 6 that the neoliberal era had eliminated all the state-owned banks but one, which he had gotten approval to expand with 2,700 new branches. Added to the existing 538 branches of the former Bansefi, that will bring the total in two years to 3,238 branches, far outstripping any other bank in the country. (Banco Azteca, currently the largest by number of branches, has 1,860.)

Digital banking will also be developed. Speaking to a local group in December, AMLO said his goal was for the Bank of the Poor to reach 13,000 branches, more than all the private banks in the country combined.

At a news conference on Jan. 8, he explained why this new bank was needed:

There are more than 1,000 municipalities that don’t have a bank branch. We’re dispersing [welfare] resources but we don’t have a way to do it. ...People have to go to branches that are two, three hours away. If we don’t bring these services close to the people, we’re not going to bring development to them…

They’re already building. I’ll invite you within two months, three at the most, to the inauguration of the first branches because they’re already working, they’re getting the land … because we have to do it quickly.

Note: This blog is based on my notes for a speech at the Harvard Class of 1957 55th reunion in Cambridge, Mass. on May 22nd.

Armageddon was threatening the financial system on Wednesday, September 17, 2008. The largest bankruptcy in American history, that of investment bank Lehman Brothers on Monday, September 15, had roiled global markets, accelerating the stupendous decline in values of every possible investment vehicle—common stocks, corporate bonds, real estate, commodities like oil, copper and gold, private equity and hedge funds alike. In the midst of the chaos Merrill Lynch, the firm that had brought Wall Street to Main Street, was absorbed in a shotgun marriage by Bank of America BAC +0%.

Only days earlier came the recognition at the New York Federal Reserve Bank and the US Treasury that AIG, the largest insurance company in the world was running out of money. This required an immediate injection of $85 billion in bail-out funds. And later another $100 billion, still not paid back to Uncle Sam.

That day, Sept 17, an even greater crisis was pending. All day long the chairman of General Electric, a company recognized across the globe as a leading industrial giant, was calling the Secretary of the Treasury, Hank Paulson to warn that the next day, Sept. 18, that GE would no longer be able to roll over its short term debt. The American business system was on the cusp of faltering mightily. The US economy was on the brink of a precipice into the unknown.

Messrs Paulson and Bernanke, at the Fed, knew the nation could not suffer the risk of a total breakdown in industry and finance. So, they decided to instantly guarantee the $600 billion commercial paper market, which is widely used to finance day-to-day operations of all major firms. This guarantee became part of the total cost of bailing out Wall Street, which totaled over $7 trillion—when you added guarantees to loans, investments and outright grants. The bailouts were key to raising the Fed’s balance sheet from $1 trillion to $3 trillion—and to upping the nation’s total amount of debt some $5 trillion to a record $15 trillion.

Conversely, the household wealth of the nation, measured by losses in financial markets and the historic drop in residential real estate—was reduced by a sickenly humungus $12-$14 trillion at the very bottom of the whole process in March, 2009. You take that money—$12-14 trillion away from the asset side of the ledger and add another $5 trillion in debt—- and you are bound to experience a decline in the nation’s GDP and a very much slower rate of recovery from such a trauma. A recovery that could take 10 years or more according to Harvard economist Kenneth Rogoff. That brings us to 2018. Need I say more?

How did we reach this very near call on a total systemic breakdown?

Firstly, there were no cops on the beat. Laissez-faire free market economics was the prevailing public policy. Federal Reserve chairman Alan Greenspan spoke of irrational exuberance but took no steps to cool off markets in the late 1990s. In fact, he was asked by Loews chairman Larry Tisch and former Goldman Sachs co-chairman John Whitehead to raise the margins on trading, and refused, claiming falsely that such a move was up to the SEC—and not the Fed. Not true.

In 1999 the Glass-Steagall Act—which had separated commercial banking from investment banking for 66 years, was overturned—a move that opened the door to more speculative trading on the part of Wall Street firms.

Then, in 2000 Messrs. Greenspan, former Treasury Secretary Rubin and his successor Lawrence Summers pressed to pass a bill that would prohibit the regulation of derivatives—the fastest growing and most complicated and murky new financial product. This was an incredible mistake, as derivative contracts like mortgage backed bonds and credit default swaps mushroomed in across the globe without any oversight, strict capital requirements and on an organized exchange where buying and selling were handled daily.

The result of this vacuum; no one anywhere knew who owed what to whom across the world. Despite the danger lurking in the rapid depreciation of these contracts, Bernanke publicly stated the absurd amount of sub-prime mortgages being sold to unsuspecting buyers would not spread to a much wider, deeper crisis. He didn’t know what he was talking about, sadly..

Lastly, in 2004 the major firms convinced the SEC to let them value certain assets on their balance sheet at values they chose—rather than marking them t o market—which would reveal what losses they were carrying. This added another dangerous laxity to financial regulation. The system was falsifying its accounts believing the investments would bounce back.

The entire catastrophe’s underlying theme was summed up later by this admission from former Fed chairman Greenspan . ” I made a mistake,” he admitted in a hearing, “in presuming that the self-interests of organizations, specifically banks and others, were such that they were best capable of protecting their own shareholders and their equity in the firms.” And we made this man into the wise parental guardian of American capitalism for 18 years. We journalists, that is.

Pressed again later on, Greenspan admitted to “shocked disbelief, (because his whole) intellectual edifice had collapsed.” Naive at minimum. At worst, locked into a narrow limited ideological viewpoint that set the stage for the meltdown. Let Goldman Sachs and Citigroup master their own appetite for profits. So much for reining in animals spirits.

Secondly, the banks and investment banks were using reckless amounts of leverage. They borrowed, in many cases, $30 to $40 of debt for every dollar of capital they had. In truth, this was a recipe for disaster, since a decline of only 4% in their capital put them on the road to insolvency. It was as if you bought a million dollar house, put down a payment of $30,000 and borrowed $970,000. What sense of irrational optimism allowed this mad way of doing business.

By the fall of 2008 the decline in the value just of subprime mortgage backed bonds—which lost up to 80% of their value in the market—meant that Fannie Mae, Freddie Mac, Lehman, Merrill Lynch, Citigroup, Bank of America, Washington Mutual and Wachovia were in a state of peril. The only way to make money in bank stocks was to short them. My favorite day trader told me after it was all over that I should be worth $50 million. With the run on Lehman Bros. both Morgan Stanley and Goldman Sachs were in danger of experiencing a run on their accounts.

Perhaps AIG is the most extreme example of leverage as financial hari-kari. It had sold protection to banks and insurance companies across the globe by issuing $540 billion of credit default swaps, which meant AIG promised to make good on any losses in value of their mortgage holdings.

LONDON, ENGLAND: Anti-Brexit campaigner Steve Bray protesting outside of the Houses of Parliament on January 30, 2020 in London, United Kingdom. At 11.00pm on Friday 31st January the UK and Northern Ireland will exit the European Union 188 weeks after the referendum on June 23rd 2016.

In 2016, Britain voted for Brexit. On Friday—four years, three prime ministers and two general elections later—the country will leave the European Union. Officially stepping out into the world is a major moment for a country that has driven itself mad on the tortuous path to the exit door. And yet, even the buildup to this historic event typified the silliest aspects of the years between the “leave” vote and the actual leaving.

Two quarrels about how Britain would mark the occasion broke out in recent weeks, one about a bell, the other about a coin. First came the fuss about whether Big Ben would ring out to mark the moment of independence. This Brexiteer wish was complicated by the fact that the bell, and the tower that houses it, are undergoing renovations, meaning a single bong would come with a $700,000 price tag. After Parliament refused to fund the move, and an online fundraising campaign failed to fill the gap, there will be no Big Ben bongs. “If Big Ben doesn’t bong, the world will see us as a joke,” lamented Brexit campaigner Nigel Farage.

A second brouhaha broke out over a commemorative 50 pence coin issued to mark the occasion. The coins, which read, “Peace, prosperity and friendship with all nations,” soon drew the ire of disbelieving Remainers. Otherwise serious and self-respecting members of the British establishment said they would refuse to use the coins or would deface any that came into their possession. (The novelist Philip Pullman also complained that the coin “is missing an Oxford comma and should be boycotted by all literate people.”)

Britain’s talent for turning these trivial rows into front-page stories illustrates how much the Brexit debate has become a negative-sum culture war, with Leavers and Remainers each compelled to take a side. Yet these dust-ups also obscure some of the more interesting, and important, divides over what Britain does with its newfound freedom. So far, much of the conversation has been backward looking, focused on whether the country would give effect to the 2016 vote with a viable version of Brexit, or whether that vote should be ignored. As Britain leaves the EU, and finally casts an eye forward, there are as many disputes as ever, with global implications, and the fault lines are more complicated than just Leave vs. Remain.

When Prime Minister Boris Johnson triumphed in last month’s election with a promise to “get Brexit done,” his opponents argued that after the sun rises on February 1, Britain’s future relationship with the EU, and a host of related questions, would remain unresolved. In a narrow sense, that claim is irrefutable. But it also misses the bigger picture.

The case for Brexit was built on possibilities. Among other things, exiting the EU allows Britain to decide for itself what trade relationships it should pursue with the rest of the world, the criteria it should set for its immigration system and how to regulate a host of areas that have been the competence of the EU for decades. These are big, difficult decisions in and of themselves. They aren’t part of a Brexit process that will ever be finished. Britain will not one day declare mission accomplished and no longer give any thought to, for example, trade policy—something that, as Americans will know, is an ongoing consideration in the politics of sovereign countries.

Understand that fact, and the divide between Leave and Remain starts to look less significant. On trade, for example, there is a split among Leavers. An image of buccaneering “Global Britain” striking trade deals with fast-growing economies around the world was a big part of the case pro-Brexit politicians made. There is little enthusiasm for this vision among Leave voters. According to one poll, Leave voters were more likely to support protectionist trade policies than Remainers. In fact, whether someone voted Leave was the single best predictor of a person’s support for barriers to trade. Politicians eager to use Brexit as an opportunity for liberalizing UK trade will have to think carefully about which voters they can rely on.

Prior to his arrest in 2003 Khodorkovsky (in photo with first Russian President Boris Yeltsin) funded several Russian parties, including the Communist Party, most of which were in competition with each other. Voltairenet.org

Prior to his arrest in 2003 Khodorkovsky (in photo with first Russian President Boris Yeltsin) funded several Russian parties, including the Communist Party, most of which were in competition with each other. Voltairenet.org

A Union Jack flag flutters in front of Big Ben as workers inspect one of its clocks, in London on Sept 11. (Reuters photo)

A Union Jack flag flutters in front of Big Ben as workers inspect one of its clocks, in London on Sept 11. (Reuters photo)

Ellen Brown is an attorney, chairman of the Public Banking Institute; author of twelve books including “Web of Debt” and “The Public Bank Solution.”

Ellen Brown is an attorney, chairman of the Public Banking Institute; author of twelve books including “Web of Debt” and “The Public Bank Solution.”