[Majorityrights Central] Explaining about life and the Reduction ad Hitlerum at The Restorationist Posted by Guessedworker on Wednesday, 13 May 2026 23:04.

[Majorityrights Central] Three possible forms of a Ukrainian victory ... and a Russian defeat Posted by Guessedworker on Thursday, 16 April 2026 16:36.

[Majorityrights Central] Empires, the Chinese Mind, a theoretical nationalism of ethnicity Posted by Guessedworker on Saturday, 14 February 2026 01:54.

[Majorityrights News] Moscow Times: Valdai residents report no sign of drones attacking Putin residence Posted by Guessedworker on Tuesday, 30 December 2025 11:33.

[Majorityrights Central] Thoughts on Mark Collett’s strategy for nationalism in the British future Posted by Guessedworker on Friday, 24 October 2025 15:01.

[Majorityrights Central] Principles, parts, processes of ethnic nationalism, Part 1: inflection? Posted by Guessedworker on Thursday, 31 July 2025 12:03.

“If you invest your tuppence wisely in the bank, safe and sound,

Soon that tuppence safely invested in the bank will compound,

And you’ll achieve that sense of conquest as your affluence expands

In the hands of the directors who invest as propriety demands.”

— “Mary Poppins,” 1964

When “Mary Poppins” was made into a movie in 1964, Mr. Banks’ advice to his son was sound. The banks were then paying more than 5% interest on deposits, enough to double young Michael’s investment every 14 years.

Now, however, the average savings account pays only 0.10% annually—that’s one-tenth of 1%—and many of the country’s biggest banks pay less than that. If you were to put $5,000 in a regular Bank of America savings account (paying 0.01%) today, in a year you would have collected only 50 cents in interest.

That’s true for most of us, but banks themselves are earning 2.4% on their deposits at the Federal Reserve. These deposits, called “excess reserves,” include the reserves the banks got from our deposits, and on which they are paying almost nothing; and unlike with our deposits, there is no $250,000 cap on the sums banks can stash at the Fed amassing interest. A whopping $1.5 trillion in reserves are now sitting in Fed reserve accounts. The Fed rebates its profits to the government after deducting its costs, and interest paid to banks is one of those costs. That means we, the taxpayers, are paying $36 billion annually to private banks for the privilege of parking their excess reserves at one of the most secure banks in the world—parking them, rather than lending them out.

The banks are getting these outsize returns while taking absolutely no risk, because the Fed, as “lender of last resort,” cannot go bankrupt. This is not true for other depositors, including large institutions such as the pension funds that hold our retirement money.

The business world has undergone considerable change in the last two decades.

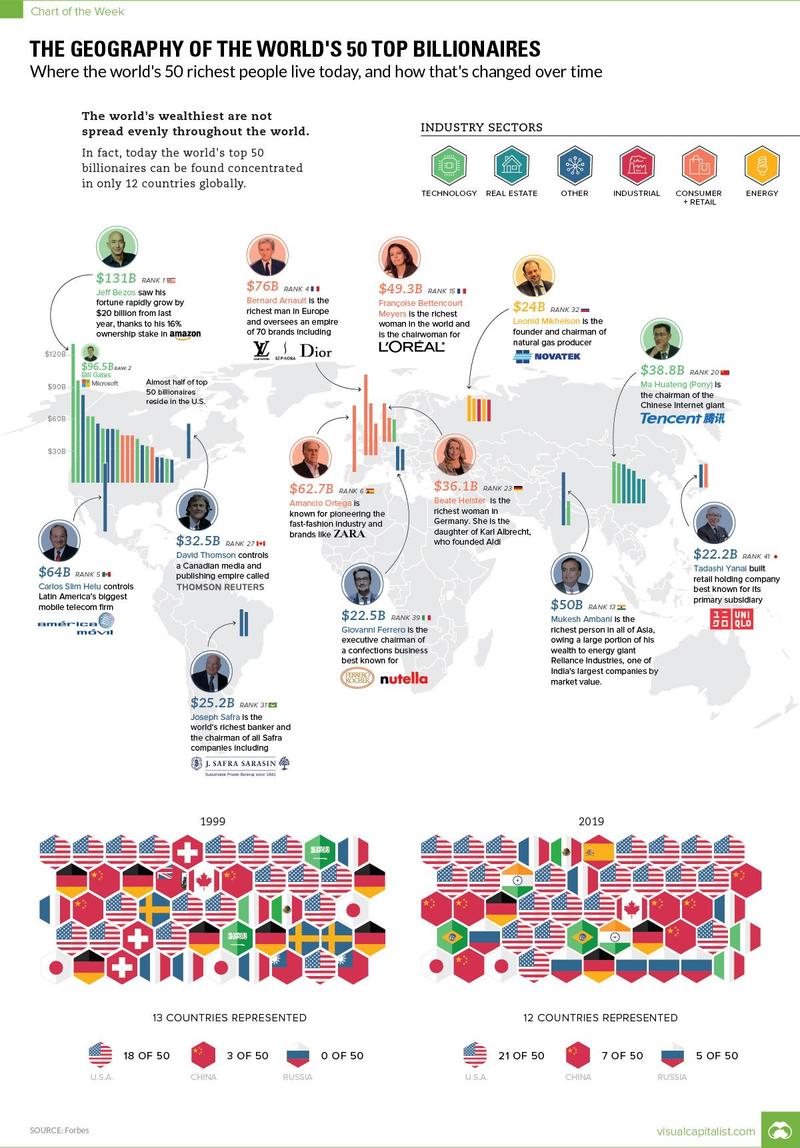

While some fortunes are always reliably passed on to their respective heirs and heiresses, Visual Capitalist’s Jeff Desjardinsnotes that there are also entirely new industries that rise out of nowhere to shape the landscape of global wealth.

As the wealth landscape shifts, so does its geographical distribution.

We’ll start here by looking at the most recent data from 2019:

The most recent billionaires list features Jeff Bezos at the top with $131 billion, although it’s likely his recent divorce announcement will provide an upcoming shakeup to the Bezos Empire.

Bezos is just one of 21 Americans that find themselves in the top 50 list, which means that 42% of the world’s top billionaires hail from the United States.

Billionaire Geography Over Time

If we compare the top 50 list to that from 1999, it’s interesting to see what has changed over time in terms of geographical distribution. Here’s the distribution of top countries on both lists, compared:

In the last 20 years, Russia and China have stockpiled the most top billionaires, adding five and four to the top 50 list respectively. The United States added three, going from 18 to 21 billionaires over the timeframe. On the other end of the spectrum, Germany, Sweden, and Switzerland have lost the most billionaires from the top 50 ranking.

Russia’s Connection To Brexit Is ‘Opaque And Complicated,’ Journalist Says, NPR, 21 Mar 2019:

Katya Banks

While there are entirely legitimate interests for Britain to leave the E.U., The Russian Federation has had an interest and potential significant influence on the leave campaign as well.

As alarm bells sound over the advancing destruction of the environment, a variety of Green New Deal proposals have appeared in the U.S. and Europe, along with some interesting academic debates about how to fund them. Monetary policy, normally relegated to obscure academic tomes and bureaucratic meetings behind closed doors, has suddenly taken center stage.

The 14-page proposal for a Green New Deal submitted to the U.S. House of Representatives by Rep. Alexandria Ocasio-Cortez, D-N.Y., does not actually mention Modern Monetary Theory (MMT), but that is the approach currently capturing the attention of the media—and taking most of the heat. The concept is good: Abundance can be ours without worrying about taxes or debt, at least until we hit full productive capacity. But, as with most theories, the devil is in the details.

MMT advocates say the government does not need to collect taxes before it spends. It actually creates new money in the process of spending it; and there is plenty of room in the economy for public spending before demand outstrips supply, driving up prices.

Critics, however, insist this is not true. The government is not allowed to spend before it has the money in its account, and the money must come from tax revenues or bond sales.

In a 2013 treatise called “Modern Monetary Theory 101: A Reply to Critics,” MMT academics concede this point. But they write, “These constraints do not change the end result.” And here the argument gets a bit technical. Their reasoning is that “the Fed is the monopoly supplier of CB currency [central bank reserves], Treasury spends by using CB currency, and since the Treasury obtained CB currency by taxing and issuing treasuries, CB currency must be injected before taxes and bond offerings can occur.”

The counterargument, made by American Monetary Institute (AMI) researchers, among others, is that the central bank is not the monopoly supplier of dollars. The vast majority of the dollars circulating in the United States are created, not by the government, but by private banks when they make loans. The Fed accommodates this process by supplying central bank currency (bank reserves) as needed, and this bank-created money can be taxed or borrowed by the Treasury before a single dollar is spent by Congress. The AMI researchers contend, “All bank reserves are originally created by the Fed for banks. Government expenditure merely transfers (previous) bank reserves back to banks.” As the Federal Reserve Bank of St. Louis puts it, “federal deficits do not require that the Federal Reserve purchase more government securities; therefore, federal deficits, per se, need not lead to increases in bank reserves or the money supply.”

What federal deficits do increase is the federal debt; and while the debt itself can be rolled over from year to year (as it virtually always is), the exponentially growing interest tab is one of those mandatory budget items that taxpayers must pay. Predictions are that in the next decade, interest alone could add $1 trillion to the annual bill, an unsustainable tax burden.

To fund a project as massive as the Green New Deal, we need a mechanism that involves neither raising taxes nor adding to the federal debt; and such a mechanism is proposed in the U.S. Green New Deal itself—a network of public banks. While little discussed in the U.S. media, that alternative is being debated in Europe, where Green New Deal proposals have been on the table since 2008. European economists have had more time to think these initiatives through, and they are less hampered by labels like “socialist” and “capitalist,” which have long been integrated into their multi-party systems.

A Decade of Gestation in Europe

The first Green New Deal proposal was published in 2008 by the New Economics Foundation on behalf of the Green New Deal Group in the U.K. The latest debate is between proponents of the Democracy in Europe Movement 2025 (DiEM25), led by former Greek finance minister Yanis Varoufakis, and French economist Thomas Piketty, author of the best-selling “Capital in the 21st Century.” Piketty recommends funding a European Green New Deal by raising taxes, while Varoufakis favors a system of public green banks.

PRIME Minister Theresa May’s Brexit deal has been rejected by the House of Commons with a 149 majority leaving the future of Britain’s exit from the bloc in complete turmoil.

A hoarse-sounding Mrs May suffered a defeat of 242/391 with a majority of 149 at tonight’s meaningful vote on her deal. She had lost her voice after a late-night flight to Strasbourg to demand concessions on her deal with European Commission president Jean Claude Juncker last night. Though it was not enough to win over both hard-line Brexiteers and MPs that back a People’s Vote. MPs could now vote to delay Brexit following an amendment by Labour’s Yvette Cooper, tabled last month, allowing them to do so.

No deal Brexit BOOST: Jacob Rees-Mogg explains ‘exception’ of no deal

Mrs May also said that “voting against a deal does not solve the issues we face”.

European Commission president Mr Juncker had already warned that if MPs turned down the package agreed in Strasbourg on Monday, there would be “no third chance” to renegotiate.

MPs will vote tomrorow on whether they want to leave the European Union without a Withdrawal Agreement and Political Declaration - a no-deal Brexit.

Should MPs reject that, there will be another vote on whether Parliament wants to seek an extension to Article 50 - delaying the UK’s departure beyond the current March 29 deadline.

But Mrs May stressed that would not resolve the divisions in the Commons and could instead hand Brussels the power to set conditions on the kind of Brexit on offer “or even moving to a second referendum”.

The essence of Slavery is that someone else controls the value of our production.

Under Capitalism, people depending on a wage (the 90/99%), typically consume only about 10% of the value of their own production. The entire System is geared to sucking up our production with unearned income: Usury, Landlordism, Speculation, high prices of Monopoly.

In Capitalism, this was achieved by first driving the common people off their ancestral lands by systematically destroying the abundant money systems of the medieval era by forcing Gold Standards everywhere.

This caused a deflation that first savaged the countryside.

In this way, the People lost their means of independence and were forced to work for others for a living, in the cities. Instead of being independent farmers and craftsmen, they were demoted to wage slavery.

By giving him a wage, immediately a large chunk of the value of the worker’s production is taken by the shareholder. The value of the worker’s production is always much higher than his wage.

With Multinationals, profits and shareholder dividends are typically higher than the cost for labor. More than half of the workers’ production is taken by the owners of the company.

Broken

They get away with this because Capital is kept artificially scarce, both through Cartels and through the artificial scarcity of money. In this way, Labor is oppressed, forcing them into low wages and humiliating conditions. With a decent monetary system, not Capital, but Labor would be the scarce factor of production, and men would be either self-employed or co-owner in larger corporations.

The worker receives his wage, and the remaining value of his production is next sucked up with scientific precision.

A wage slave making $2000 per month has a budget something like this: $300 for the State $700 for the Landlord $100 for Energy $200 for ‘health’ ‘care’ $150 for Transportation $50 for Telecom Total: $1500

What remains, $500, about a quarter, is to eat and try to live a life. A fraction of what 40 hours work produced, at least $4000 worth.

The beauty of the System is, that when wages rise, prices, debts (and associated usurious cost), rents, rise along, sucking up the extra purchasing power.

The residual wealth that the Middle Class retains during booms is disowned a little later with the inevitably following crunch, forcing them into liquidation at depressed prices.

Free Markets, Right?! Supply and demand! All good and dandy, we think. Fair enough. We use stuff, so we pay.

But when we take a closer look at where all this money ends up, it transpires that all supply chains we depend on (energy, automotive industry, telecom, ‘health’ ‘care’) are dominated by massive International Cartels.

Cartels keep supply low, and prices high, so a lot of their profits are unearned income, not really related to their production, but to their market power. They use this to keep competitors out, and the Capitalist’s core value is ‘Competition is Sin’ (John D. Rockefeller).

LANDLORDISM

What is more, a great many people are enslaved by Landlordism, which is a vicious Tyranny, first established by the Sword, later overtaken by mortgages, the Money Power’s method of disowning the Landed Aristocracy.

Landlordism is pure parasitism, and all the Land is owned by a really very small group of mostly very old families. For instance: all the homeowners in Britain combined own only 6% of the Land. All the rest is in the hands of a minute percentage of the population. Many of the main Landholders go back all the way to William the Conqueror.

Filthy rich

Usury massively raises all these prices. As we know, Usury is about 40% of prices we pay for all goods and services: cost for capital passed on by the supplier.

This includes the land we live on, and on which we are utterly dependent. In fact, Usury actually QUADRUPLES Landlordism´s rents.

But this is not the only way International Finance profits from everything: they also have a decisive stake in most of the Transnationals that dominate the supply chains we are completely dependent upon. Only 20% of Transnationals (there are about 40,000 of them) are independently owned.

CONCLUSION

In the past, people enslaved in the mines and the sweatshops, say late 19th century Britain, they were even forced by their employers to do their groceries in factory owned shops that charged outrageous prices.

We think we have outgrown this. It’s really time to think again: all that has happened is that Capital (Finance) has upped their game. Local shops on factory compounds are now international supermarket chains. But they are owned by the same people and serve the exact same purpose: reclaiming capital’s losses to wages, usurping our production.

People even go so far as to say ‘Capitalism has lifted people out of poverty’! What is so insane about this, is that a man, in 1694, worked about 15 weeks per year on his own farm. Then with the ascent of Capitalism, two centuries later, he worked 80 hours per week in some soul-crushing ‘job’, and it was still not enough: his wife and his kids had to work too, just to pay for the rent and some potatoes.

Anthony Migchels

Even today, we work at least twice as much as three centuries ago.

The most galling of it all is that people claim ‘freedom’ because once every four years they get to give what remains of their power away to some Kleptocrat insider with ‘democratic elections’.

This is the reality of Capitalism, which is centred around International Finance and its Usury (Banking).

No solution to all this is thinkable, without the end of Usury by interest-free credit for the People.

Posted by DanielS on Saturday, 09 February 2019 07:49.

TruthDig.Org., “The Venezuela Myth Keeping Us From Transforming Our Economy”, 7 Feb 2019:

Modern Monetary Theory (MMT) is getting significant media attention these days, after Rep. Alexandria Ocasio-Cortez said in an interview that it should “be a larger part of our conversation” when it comes to funding the “Green New Deal.” According to MMT, the government can spend what it needs without worrying about deficits. MMT expert and Bernie Sanders adviser professor Stephanie Kelton says the government actually creates money when it spends. The real limit on spending is not an artificially imposed debt ceiling but a lack of labor and materials to do the work, leading to generalized price inflation. Only when that real ceiling is hit does the money need to be taxed back, but even then it’s not to fund government spending. Instead, it’s needed to shrink the money supply in an economy that has run out of resources to put the extra money to work.

Predictably, critics have been quick to rebut, calling the trend to endorse MMT “disturbing” and “a joke that’s not funny.” In a Feb. 1 post on the Daily Reckoning, Brian Maher darkly envisioned Bernie Sanders getting elected in 2020 and implementing “Quantitative Easing for the People” based on MMT theories. To debunk the notion that governments can just “print the money” to solve their economic problems, he raised the specter of Venezuela, where “money” is everywhere but bare essentials are out of reach for many, the storefronts are empty, unemployment is at 33 percent and inflation is predicted to hit 1 million percent by the end of the year.

Blogger Arnold Kling also pointed to the Venezuelan hyperinflation. He described MMT as “the doctrine that because the government prints money, it can spend whatever it wants . . . until it can’t.” He said:

To me, the hyperinflation in Venezuela exemplifies what happens when a country reaches the “it can’t” point. The country is not at full employment. But the government can’t seem to spend its way out of difficulty. Somebody should ask these MMT rock stars about the Venezuela example.

I’m not an MMT rock star and won’t try to expound on its subtleties. (I would submit that under existing regulations, the government cannot actually create money when it spends, but that it should be able to. In fact, MMTers have acknowledged that problem; but it’s a subject for another article.) What I want to address here is the hyperinflation issue, and why Venezuelan hyperinflation and “QE for the People” are completely different animals.

What Is Different About Venezuela

Venezuela’s problems are not the result of the government issuing money and using it to hire people to build infrastructure, provide essential services and expand economic development. If it were, unemployment would not be at 33 percent and climbing. Venezuela has a problem the U.S. does not, and will never have: It owes massive debts in a currency it cannot print itself, namely, U.S. dollars. When oil (its principal resource) was booming, Venezuela was able to meet its repayment schedule. But when the price of oil plummeted, the government was reduced to printing Venezuelan bolivars and selling them for U.S. dollars on international currency exchanges. As speculators drove up the price of dollars, more and more printing was required by the government, massively deflating the national currency.

It was the same problem suffered by Weimar Germany and Zimbabwe, the two classic examples of hyperinflation typically raised to silence proponents of government expansion of the money supply before Venezuela suffered the same fate. Professor Michael Hudson, an actual economic rock star who supports MMT principles, has studied the hyperinflation question extensively. He confirms that those disasters were not due to governments issuing money to stimulate the economy. Rather, he writes, “Every hyperinflation in history has been caused by foreign debt service collapsing the exchange rate. The problem almost always has resulted from wartime foreign currency strains, not domestic spending.”

Venezuela and other countries that are carrying massive debts in currencies that are not their own are not sovereign. Governments that are sovereign can and have engaged in issuing their own currencies for infrastructure and development quite successfully. I have discussed a number of contemporary and historical examples in my earlier articles, including in Japan, China, Australia and Canada.

Although Venezuela is not technically at war, it is suffering from foreign currency strains triggered by aggressive attacks by a foreign power. U.S. economic sanctions have been going on for years, causing the country at least $20 billion in losses. About $7 billion of its assets are now being held hostage by the U.S., which has waged an undeclared war against Venezuela ever since George W. Bush’s failed military coup against President Hugo Chávez in 2002. Chávez boldly announced the “Bolivarian Revolution,” a series of economic and social reforms that dramatically reduced poverty and illiteracy as well as improved health and living conditions for millions of Venezuelans. The reforms, which included nationalizing key components of the nation’s economy, made Chávez a hero to millions of people and the enemy of Venezuela’s oligarchs.

Nicolás Maduro was elected president following Chávez’s death in 2013 and vowed to continue the Bolivarian Revolution. Recently, as Saddam Hussein and Moammar Gadhafi had done before him, he defiantly announced that Venezuela would not be trading oil in U.S. dollars following sanctions imposed by President Trump.

The notorious Elliott Abrams has now been appointed as special envoy to Venezuela. Considered a war criminal by many for covering up massacres committed by U.S.-backed death squads in Central America, Abrams was among the prominent neocons closely linked to Bush’s failed Venezuelan coup in 2002. National security adviser John Bolton is another key neocon architect advocating regime change in Venezuela. At press conference on Jan. 28, he held a yellow legal pad prominently displaying the words “5,000 troops to Colombia,” a country that shares a border with Venezuela. Clearly, the neocon contingent feels it has unfinished business there.

Bolton does not even pretend that it’s all about restoring “democracy.” He blatantly said on Fox News, “It will make a big difference to the United States economically if we could have American oil companies invest in and produce the oil capabilities in Venezuela.” As President Nixon said of U.S. tactics against Salvador Allende’s government in Chile, the point of sanctions and military threats is to squeeze the country economically.

Killing the Public Banking Revolution in Venezuela

It may be about more than oil, which recently hit record lows in the market. The U.S. hardly needs to invade a country to replenish its supplies. As with Libya and Iraq, another motive may be to suppress the banking revolution initiated by Venezuela’s upstart leaders.

The banking crisis of 2009–10 exposed the corruption and systemic weakness of Venezuelan banks. Some banks were engaged in questionable business practices. Others were seriously undercapitalized. Others still were apparently lending top executives large sums of money. At least one financier could not prove where he got the money to buy the banks he owned.

Rather than bailing out the culprits, as was done in the U.S., in 2009 the government nationalized seven Venezuelan banks, accounting for around 12 percent of the nation’s bank deposits. In 2010, more were taken over. Chávez’s government arrested at least 16 bankers and issued more than 40 corruption-related arrest warrants for others who had fled the country. By the end of March 2011, only 37 banks were left, down from 59 at the end of November 2009. State-owned institutions took a larger role, holding 35 percent of assets as of March 2011, while foreign institutions held just 13.2 percent of assets.

Brexit Horror: Remainers plot take-over.

Brexit Horror: Remainers plot take-over.

Abolished

Abolished Broken

Broken Filthy rich

Filthy rich Anthony Migchels

Anthony Migchels